The reallocation from public to private markets has been one of the most significant portfolio rotations of the past decade.

After a 2022 that saw a rapid sell-off in public equity and debt markets, some asset owners—such as many US state pension plans—find themselves overweight private assets versus targets. Should that allocation increase further? It's one of the most pressing strategic-allocation issues today. In our view, there's a case for private asset allocations to continue rising, but it's become more nuanced.

Several forces have been behind the run-up in private market exposures over the past decade. On the demand side, investors responded to low return expectations across asset classes and a need for diversifiers, enabled by a plentiful supply of liquidity from central banks. There was a supply-side element too: the stock of public equity declined (the price rose, but the number of shares fell), and banks retreated from providing credit. These supply and demand forces remain in place today.

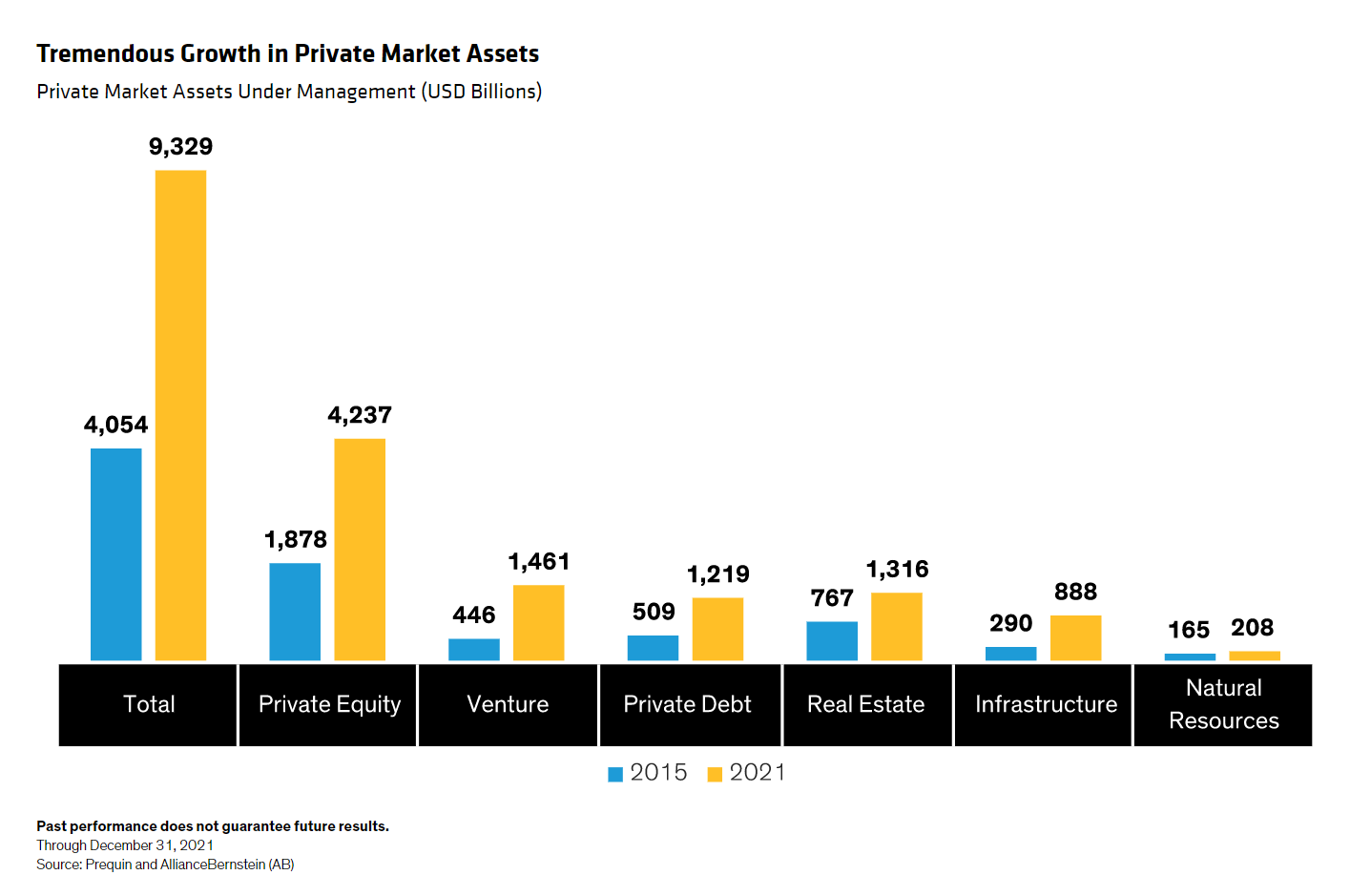

Pulling the historical lens back a bit further, assets under management in private markets have seen tremendous growth over the past 20 years—from less than US$1 trillion in the early 2000s to more than US$9.3 trillion in the second half of 2021. From 2015 to 2021, growth was particularly strong, at a nearly 15% annualized rate. Venture capital led the way, with 22% annualized growth (Display), followed by private infrastructure at 20.5% and private debt at 15.7%.

A Radically Different Macro Backdrop…and a Painful Epiphany

The role of private assets in asset allocations can't be determined in isolation, because the macro backdrop is a key force at work. In our view, the post-pandemic world presents a new macro equilibrium that demands a response. Many investors (those with real, or inflation-adjusted, liabilities) face a painful reality in terms of a lower real Sharpe ratio than they could achieve over the past four decades.

There are different moving parts to this conclusion, including these key elements:

- Inflation is likely to find a strategic equilibrium above the pre-pandemic level, raising the bar for the ability to maintain purchasing power.

- The growth outlook is lower than the norms of recent decades, with the added effect of declining corporate margins.

- A case can be made for a higher level of volatility ahead.

- Bonds are less likely to be as effective a diversifier—2022 should have been a wake-up call to investors on this point.

- Active management will play a greater role in a world where markets are less trend-driven and returns from passive betas are lower.

Revisiting the Case for More Private Asset Exposure

Private assets have been popular because they meet investor demand to access different types of return streams to fill out portfolio allocations—a response to the prospect of lower-than-average returns and a pressing need for diversification.

But what is one paid for holding private assets, and what risks are being taken on in return for the advantages these assets may bring? The traditional answer: private assets provide an illiquidity premium, which should be an important portfolio component for investors with longer horizons. There's an intense focus today, of course, on whether that illiquidity premium still exists across all subdivisions of private assets. In private equity, for instance, we're not sure it does, in aggregate.

Some areas of private markets also provide investors with access to segments of the economy that aren't well represented in public markets. This is particularly relevant in the case of infrastructure, some segments of private debt, real estate and natural resources. The benefit of control has long been an important claim in the case for private assets, though we won't discuss the ability to prove this benefit or not at a single asset- or fund-level here.

Instead, we make the macro case that there's more appetite for an active approach in a world where returns from long-only passive "betas" are lower, markets are less trend driven and the business cycle has reasserted itself. This environment makes active return streams likely to become a bigger part of end clients' return streams, and private assets naturally play an important role in this context.

For example, private equity includes the ability to determine corporate policy, and private debt the ability to manage through a potential default cycle. It would be misguided to assume that private assets have a monopoly on active returns, but they are part of an overall active allocation.

The quest for diversification has also influenced the march toward greater private exposure. One of the big shocks of 2022 was the comprehensive failure of high-grade bonds to diversify equity risk. We think investors have to get used to this state—it implies a big shift in perspective and portfolio design, with sources of diversification becoming a larger preoccupation. This diversification must be viewed in the context of unstitching the "fake" diversification of not marking to market from the more useful diversification derived from exposure to areas of the economy that are hard to buy in public markets.

Supply reasons are driving the growing adoption of private assets, too, in part because traditional lenders have stepped away from credit provision. In the US, all net growth in credit provision over the past decade has come from nontraditional lenders. In a similar vein, there's been a decline in the amount of listed equity in developed markets (Display). The total market cap of the US stock market, and indeed of the developed world, has increased, but only because of rising prices. Buybacks have exceeded issuance, and the stock of shares in circulation has declined.

The MSCI All-Country World Index has seen a slight increase in the number of shares stemming from positive net issuance in emerging markets, but there's been a marked lack of new supply even for that broader index compared with previous decades. Holding other things equal, an asset owner who wants to earn equity or credit premia should have a larger allocation to private markets today than 20 years ago. This argument for net supply driving demand for private equity and credit doesn't apply to government securities, where there's a super-abundance of supply.

This post is funded by AllianceBernstein

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.