A global economic outlook for fractured alliances, fiscal strain, and massive-scale AI investment could drive divergent possibilities – and reward diversified, high quality fixed income and credit strategies.

The world today is undergoing a rupture. Fragmentation is becoming evident around the world in energy prices, supply chain data, growth rates, and investment returns. The cost of complacency has surged. Investors can no longer rely on outdated assumptions about globalisation, policy backstops, and suppressed volatility.

Yet, as we assess the structural forces that will shape the global economy and markets over the next five years in our latest Secular Outlook, investment opportunities remain abundant.

In a world characterised by rupture – geopolitical, economic, and institutional – the case for building resilient portfolios without reaching for risk is stronger today than it has been in years.

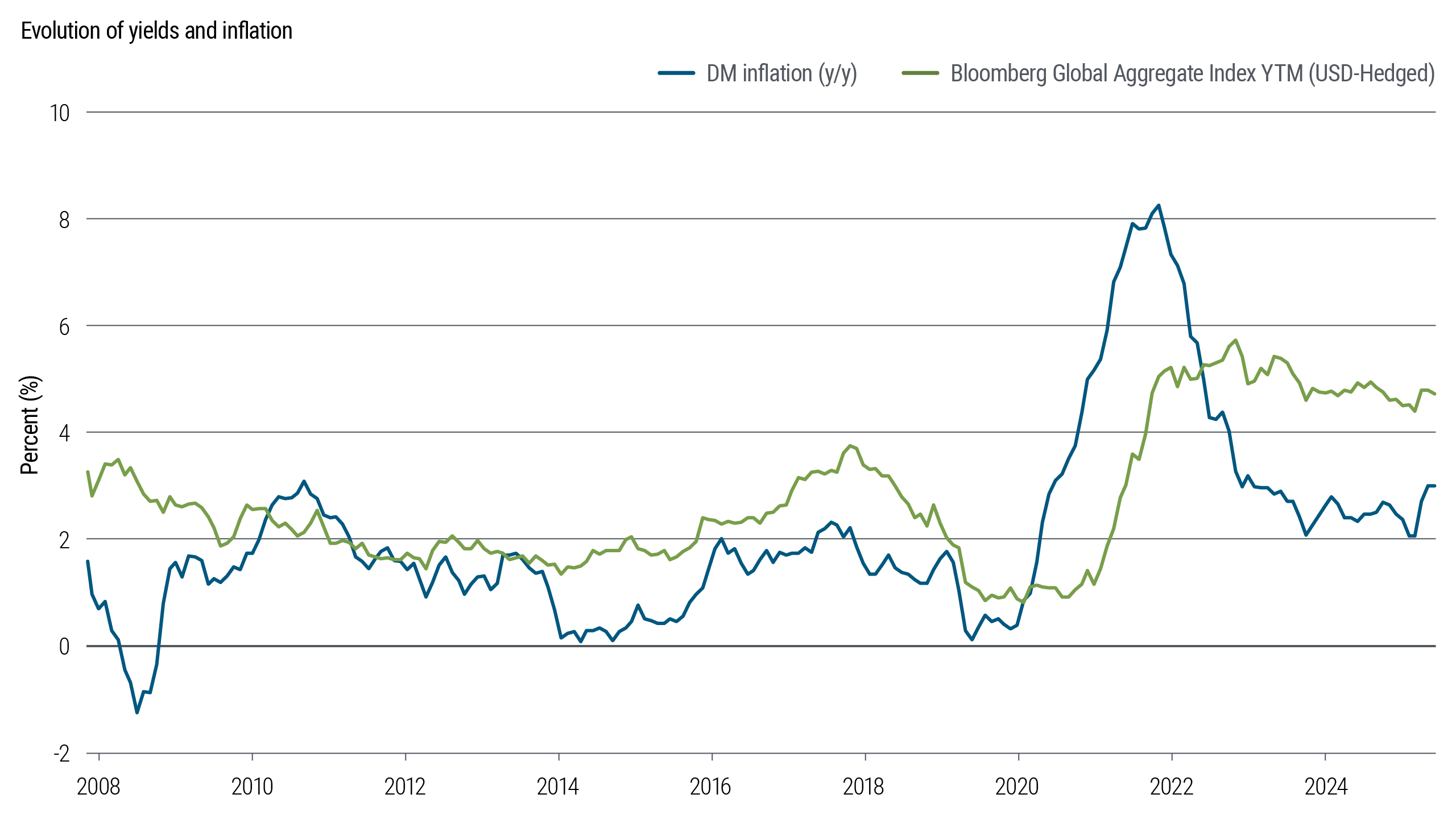

The low-yield era following the global financial crisis was a historical anomaly. The reset in global yields over the past several years (see Figure 1) has restored fixed income's role as both a return generator and a shock absorber, at a time when equity valuations and private market leverage leave less margin for error.

Figure 1: Fixed income yields remain compelling and signal attractive return potential

Source: Bloomberg, PIMCO as of 31 May 2026. Data shown are yield to maturity (YTM) of the Bloomberg Global Aggregate Index, and year-over-year inflation of developed market (DM) economies, GDP-weighted across U.S., eurozone, Japan, U.K., Canada, Australia, New Zealand, Sweden, Norway, Denmark, and Switzerland.

This greater yield "cushion" can provide bonds a secular advantage, with the opportunity for strong performance across a wide variety of potential scenarios:

· Deflationary pressures arising from AI-related efficiency gains

· A potential disappointment in AI-related efficiency gains that slows equity-led economic gains

· Growth shocks that lead to central bank rate cuts

In the past, bond investors often had to choose between desirable characteristics such as attractive yield, high credit quality, and diversification benefits. Today, investors may be able to realise these attributes together.

The defining investment implication of our secular outlook is not that risk should be avoided, but that investors should be paid for risk – and that investors no longer need to stretch to achieve reasonable long-term returns. High quality fixed income may once again offer income levels competitive with long-run equity returns, with materially lower volatility and strong potential across a variety of scenarios, particularly in a downturn. In an environment of fatter tails, that matters.

Fixed income's value proposition, in absolute and relative terms

Over multiyear horizons, fixed income returns have historically been largely anchored by starting yields. Today, those starting yields look compelling. The yields on the Bloomberg U.S. Aggregate and Global Aggregate (hedged to U.S. dollar) indices, two common benchmarks for high quality bonds, are about 4.71% and 4.75%, respectively, as of 4 June 2026.

Using that as a baseline, managers with global mandates can construct diversified portfolios yielding 5%–7% in local-currency terms without necessarily compromising quality or liquidity. Bond yields continue to appear more attractive relative to cash for a modest increase in risk.

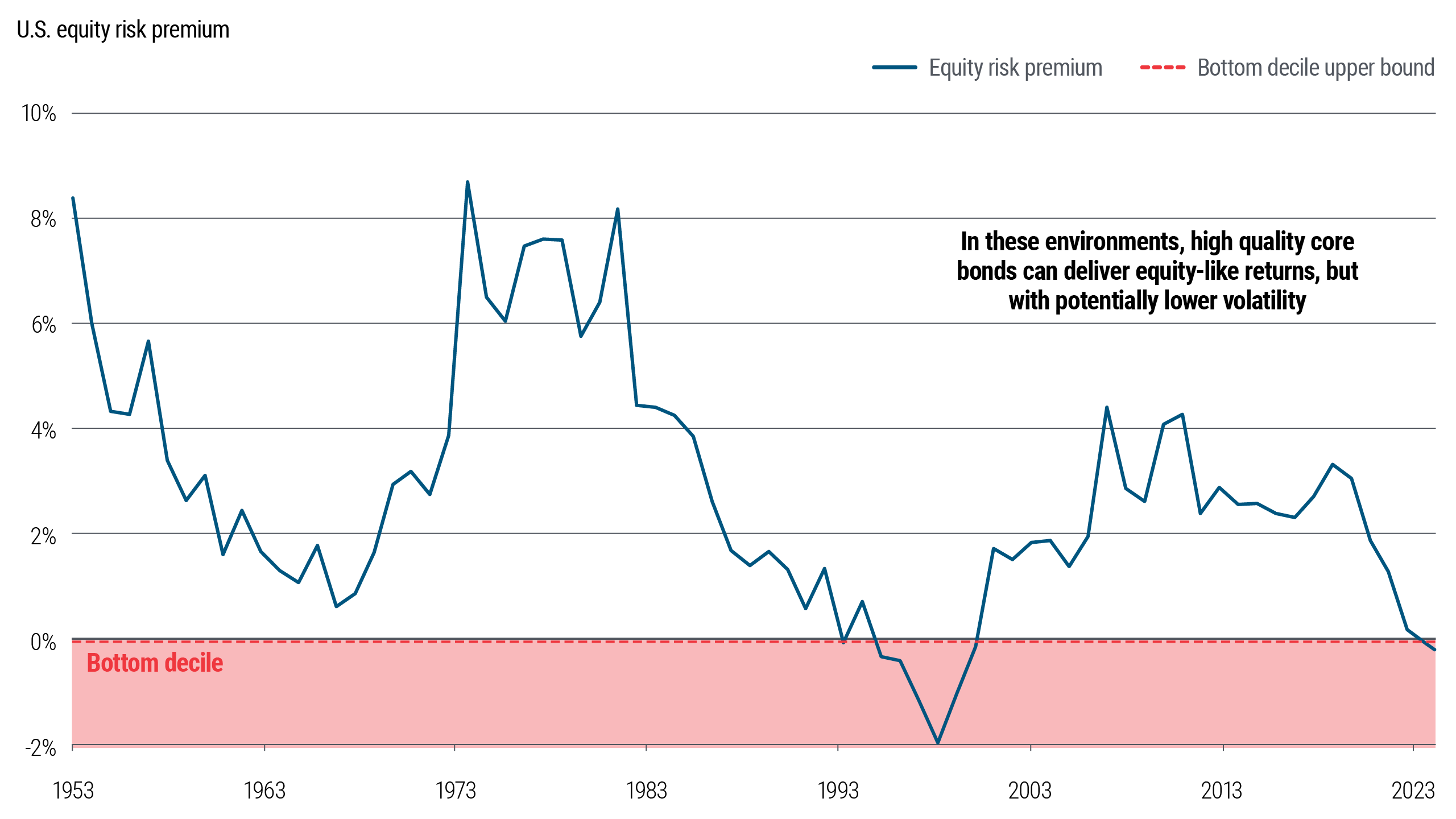

The comparison with equities is increasingly stark. Equity valuations remain elevated relative to history, and the equity risk premium – particularly in the U.S. – sits near the low end of its post–World War II range (see Figure 2).

Figure 2: Equity valuations remain stretched, with U.S. equity risk premium near zero

For Illustrative Purposes Only. Source: Bloomberg data, PIMCO calculations as of 30 April 2026.

We are not calling for an imminent equity correction. But we do believe that the prospective Sharpe ratio – a gauge of risk-adjusted return – of high quality fixed income now compares favourably with equities for the first time in many years. This argues for reconsidering portfolio allocations that were shaped during the low-yield, low-volatility decade following the global financial crisis.

We continue to believe that the traditional 60/40 stocks/bonds framework again warrants attention after equity exposures for many investors have drifted higher. Fixed income can once again do more of the work it was always meant to do: generate income, dampen volatility, and provide ballast during risk-off episodes.

High quality fixed income: where the opportunity sits

Within high quality fixed income, our highest-conviction opportunities remain concentrated in a few areas.

First, intermediate-duration bonds. The five- to 10-year segment of global yield curves looks well compensated relative to both shorter-dated cash and the long end, where fiscal dynamics and term premium uncertainty argue for caution.

Second, agency mortgage-backed securities stand out. These securities trade in a deep and liquid market. Spreads remain wide relative to history, credit quality is high, and supply/demand dynamics are improving as bank balance sheets stabilise and the Federal Reserve's footprint recedes. In our view, this combination can offer an attractive source of income and diversification.

Third, global government bonds merit renewed attention. Business cycles are increasingly desynchronised, and monetary policy paths are diverging across countries. A global fixed income allocation can seek the potential benefits of global diversification and strengthened risk-adjusted returns over time. It can create opportunities for active country selection – including EM countries with credible policies and strong fundamentals – and curve positioning that were largely absent during the era of synchronised global easing. At today's starting yields, global bond exposure should help provide diversification alongside the potential for higher income. With the U.S. on an unsustainable long-term debt path, owning non-U.S. debt can be a prudent way to diversify.

Finally, inflation-linked bonds and select real assets often play an important role in resilient portfolios. With inflation tails fatter and geopolitical risks to energy elevated, real (inflation-adjusted) yields that are positive by historical standards can help provide a meaningful buffer to volatility. Gold, in particular, has continued to serve as a neutral store of value in a world of partial confidence in fiat currencies.

Credit: the dispersion is the opportunity

Credit markets, in aggregate, continue to price a benign outcome. Credit spreads across investment grade, high yield, and private credit remain near the tight end of historical distributions despite elevated secular uncertainty. We interpret this as complacency rather than strength.

We are particularly cautious in lower-quality, economically sensitive corporate credit. Years of abundant capital and "buy the dip" behaviour have encouraged aggressive underwriting, high leverage, and widespread use of floating-rate structures.

As growth slows and refinancing costs remain elevated, stresses are emerging – most visibly in segments of private corporate credit and middle market direct lending. We are witnessing increased instances of maturity extensions and payment-in-kind structures that allow borrowers to repay debt with more debt. In our view, a more genuine default cycle is now unfolding, and investors should not expect past patterns of rapid recovery to repeat with the same reliability.

By contrast, we continue to see more attractive risk-adjusted opportunities in asset-based finance. Areas such as equipment finance, consumer lending, residential mortgages, real estate credit, and select infrastructure finance benefit from strong collateral, granular diversification, and cash flows that are less directly tied to corporate earnings. At current valuations, these characteristics can offer what we see as a superior balance of income and source of downside protection.

Opportunities across EM

The starting yields available today across EM local and hard currency markets are among the most compelling in over a decade. There is also potential for secular U.S. dollar weakness, historically among the most powerful tailwinds for EM local currency returns.

In today's macro backdrop EM now provides important portfolio diversification against the very disruptions emanating from the developed world itself. In a regime where U.S. fiscal dynamics, dollar rebalancing, and DM policy uncertainty are the primary sources of portfolio risk, EM exposure can offer a genuine hedge rather than simply an additional source of yield.

Putting it together

In a post-rupture world, the most consequential investment mistake is reaching for risk when that risk is poorly compensated. We believe the current yield environment offers a compelling alternative.

We believe resilient portfolios today are built around liquid, high quality fixed income, an up-in-quality bias in credit, broad global diversification, and selective exposure to real assets and asset-based finance. Over the next five years, discipline is likely to matter more than daring – and resilience more than reach.

Disclosures

Past performance is not a guarantee or a reliable indicator of future results.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be appropriate for all investors. The value of real estate and portfolios that invest in real estate may fluctuate due to: losses from casualty or condemnation, changes in local and general economic conditions, supply and demand, interest rates, property tax rates, regulatory limitations on rents, zoning laws, and operating expenses. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and their value may fluctuate in response to the market's perception of issuer creditworthiness; while generally supported by some form of government or private guarantee, there is no assurance that private guarantors will meet their obligations. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Management risk is the risk that the investment techniques and risk analyses applied by an investment manager will not produce the desired results, and that certain policies or developments may affect the investment techniques available to the manager in connection with managing a strategy.

Investments in asset-based lending and asset-backed instruments are subject to a variety of risks that may adversely affect the performance and value of the investment. These risks include, but are not limited to, credit risk, liquidity risk, interest rate risk, operational risk, structural risk, sponsor risk, monoline wrapper risk, and other legal risks. Asset-backed securities across various asset classes may not achieve business objectives or generate returns, and their performance can be significantly impacted by fluctuations in interest rates. Investments in residential and commercial mortgage loans, as well as commercial real estate debt, are subject to risks that include prepayment, delinquency, foreclosure, risks of loss, servicing risks, and adverse regulatory developments. These risks may be heightened in the case of non-performing loans. Structured products, such as collateralised debt obligations, are also highly complex instruments that typically involve a high degree of risk; the use of these instruments may involve derivative instruments that could result in losses exceeding the principal amount invested. Private credit involves investments in non-publicly traded securities, which may be subject to illiquidity risk. Portfolios that invest in private credit may be leveraged and may engage in speculative investment practices that increase the risk of investment loss. Additionally, investments in private credit may be subject to real estate-related risks, which include new regulatory or legislative developments, the attractiveness and location of properties, the financial condition of tenants, potential liability under environmental and other laws, as well as natural disasters and other factors beyond a manager's control. Investing in banks and related entities is a highly complex field subject to extensive regulation, and investments in such entities may give rise to control person liability and other risks. Investing in distressed loans and bankrupt companies is speculative, and the repayment of default obligations contains significant uncertainties. High-yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Collateralised Loan Obligations (CLOs) may involve a high degree of risk and are intended for sale to qualified investors only. Investors may lose some or all of their investment, and there may be periods during which no cash flow distributions are received. These investments are exposed to risks such as credit, default, liquidity, management, volatility, interest rate, and credit risk.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

For professional use only

Per the information available to us you fulfil the requirements to be classified as professional clients as defined in the MiFiD II Directive 2014/65/EU Annex II Handbook. Please inform us if otherwise. The services and products described in this communication are only available to professional clients as defined in the MiFiD II Directive 2014/65/EU Annex II Handbook and its implementation of local rules and as defined in the Financial Conduct Authority's Handbook. This communication is not a public offer and individual investors should not rely on this document. Opinion and estimates offered constitute our judgement and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

PIMCO Europe Ltd (Company No. 2604517, 11 Baker Street, London W1U 3AH, United Kingdom) is authorised and regulated by the Financial Conduct Authority (FCA) (12 Endeavour Square, London E20 1JN) in the UK. The services provided by PIMCO Europe Ltd are not available to retail investors, who should not rely on this communication but contact their financial adviser. Since PIMCO Europe Ltd services and products are provided exclusively to professional clients, the appropriateness of such is always affirmed.

CMR2026-0604-5550145