Royal London Asset Management (RLAM) investment director Jonathan Price shares how the team’s Life Cycle approach helps their portfolios stand out.

What trends and developments are you seeing in the global equity market?

It's been turbulent obviously. What was initially referred to as 'transient inflation' turned out to be much more persistent. As a result, central banks have begun to raise rates in the face of growing pressure.

One of the consequences is that the value of future cash flows is diminished compared with today. During the first half of this year this hit a lot of stocks priced on future growth.

July saw a reversal of this as sentiment moved towards a medium-term outlook of inflationary control, rates stabilisation and subsequent fall and a soft economic landing.

Whist this is a plausible scenario, there's an equally plausible alternative of problematic inflation control, further significant rate rises and a sharp economic recession. These scenarios have quite different outcomes for risk assets like equities.

Do these trends influence the way RLAM invests?

It may be that the volatility posed by these conflicting scenarios is presenting a significant opportunity for stock pickers as prices have been fluctuating widely. That said, positioning for either one of these scenarios is not a return driver for the portfolios but rather a risk mitigating challenge. The biggest risk exposures of our portfolios and the drivers of performance over 20 plus years running a global equity process are very much stock specific, meaning that our non-stock risk exposures i.e. style, region, sector, currency, commodity, interest rate sensitivity etc are residual risks that we try to minimise rather than call.

For us, it's all about finding, from an incredibly broad and rich universe, individual companies with shareholder wealth creation potential at attractive valuations.

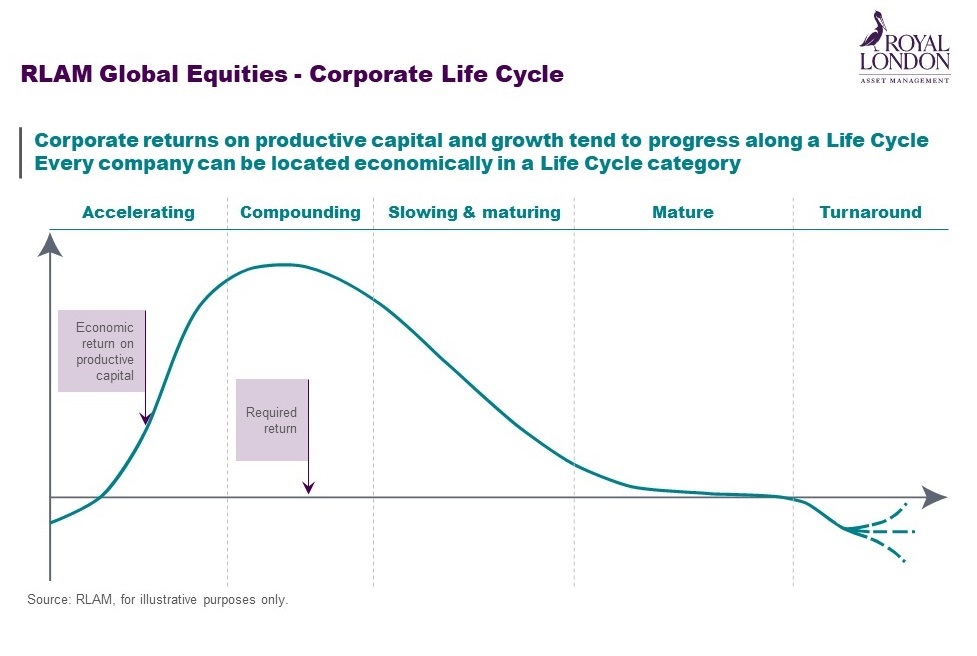

One of our differentiating features in this regard is the use of a Life Cycle framework to apply our edge in finding these opportunities.

The framework is based on the belief that all corporates go through what we've defined as five stages of life: from early accelerating, to compounding, slowing and maturing, mature and eventually turning around.

This approach does two things. The first is to inform the path of our analysis, meaning that whilst we believe you can potentially invest successfully at any stage of the Life Cycle, the things that we look for are quite different in each stage. Specifically, what makes a winning (or losing) accelerator is quite different to what makes a winning (or losing) turnaround.

The second thing is that it's a pillar of our diversification strategy. We seek to maximise exposure to stock specific risk and so minimise other factors like style, interest rate, currency, region, sector etc and Life Cycle diversification is a big part of that.

As a result, we've been able to perform across different market cycles and environments in our core strategies, including the periods pre, during and post Covid.

So how does the Global Equity Sustainable Transition strategy complement your existing range and what makes it different?

The Global Equity investment approach has always integrated ESG analysis as a core element of the investment process as the team believes that this can lead to investment advantages. ESG integration is owned and conducted by the investment team as an integral part of analysis. This analysis is supported by the expertise and advice from RLAM's Responsible Investment team. ESG integration is involved at both key stages of the stock selection process: Shareholder Wealth Creation, where assessment of ESG risks/opportunities and subsequent ESG analysis is an explicit part of the scorecard informing the overall wealth creation assessment and valuation analysis where ESG factors are explicitly incorporated into our cash flow forecasts.

We were being increasingly asked whether these insights could be extended to a proposition that was tasked with delivering not just performance, but performance with real specific purpose.

The specific purpose in question here is the transition to sustainability and what makes this strategy different to many is the focus on the ‘change' (i.e. the transition) rather than just the ‘level' of sustainability.

It's about putting money to work for that change, investing in companies that are either themselves transitioning (improvers) or helping others to do so (enablers). That dynamic is important. The world is currently on an unsustainable path so simply avoiding companies with sustainability challenges won't drive meaningful change.

So, to answer the question specifically, the complement between this and our other strategies is each stock in the portfolio comes through the same Life Cycle driven process that identified stocks with attractive shareholder wealth creation potential and valuations. The major difference is that on top of this, each holding will have a material and credible investment transition thesis that we adhere to, continuously evaluate, and engage on.

We've grouped the types of transition we are looking for into four main themes: Climate Stability, Natural Capital Preservation, Health and Wellbeing and Equality of Opportunity. Each of which relate to one or more of the UN Sustainable Development Goals and every company in the portfolio is an improver or enabler (or both) in one or more of these themes.

What are the key features of this Sustainable Transition strategy?

First: financial performance is driven by a process that's delivered for 20 years over a number of investment and market cycles.

Second: we believe that the process approach of Life Cycle diversification lowers the style risk that is often associated with strategies in the universe - ‘Growth' tends be associated with the front end of the Life Cycle, ‘Value' with the back end.

Third: every stock has a material contribution to one or more sustainable transitions themes, making a difference for tomorrow rather than avoiding challenges today. And last, Engagement is investor-led and used to hold the companies we invest in to account.

What would you say are the challenges and opportunities of moving to a sustainable approach?

For clients, the first challenge is increasingly one of choice - which is a good thing. Sustainability is a fast-broadening category that is moving mainstream. Clients are going to need to take a view not only on a manager's ability to deliver financial objectives (a challenge they are used to) but also the type of non-financial purpose they want to be associated with and the materiality and credibility of that.

The second challenge is understanding and incorporating how this non-financial purpose might affect the financial performance and vice versa. For example, does migration to a more sustainable strategy introduce an investing style or any other top-down bias? What are the potential effects of exclusions over different cycles? None of this is necessarily a bad thing in the long run but needs to be understood and incorporated into expectations. For example, many of the strategies that are ‘green' today come with a quality growth bias built in given the nature of the companies included e.g. tech firms. That's been a big tailwind for the last few years, but they have struggled in the market rotation.

The third challenge, which is as much for the manager as the client, is regulation and reporting. In terms of regulation, things are changing unbelievably fast, both at an investment and at company level. But there are still huge gaps in reporting, whether it be companies themselves operating to different statutory standards and timelines, or investment managers working through latest fund requirements. Ultimately reporting in terms of measurements and metrics is a blunt tool given these factors and managers will need to work hard with clients to bring to life how their investments are both delivering a financial return and making a difference in the world.

For more information on RLAM's range of investment capabilities and services please visit www.rlam.com

Past performance is not a guide to future performance. The value of investments and any income from them may go down as well as up and is not guaranteed. Investors may not get back the amount invested. The views expressed are those of the author at the date of publication unless otherwise indicated, which are subject to change, and is not investment advice.

For Professional Clients only, not suitable for Retail Clients.

This is a financial promotion and is not investment advice. Telephone calls may be recorded. For further information please see the Privacy policy at www.rlam.com

Issued in September 2022 by Royal London Asset Management Limited, 55 Gracechurch Street, London, EC3V 0RL. Authorised and regulated by the Financial Conduct Authority, firm reference number 141665. A subsidiary of The Royal London Mutual Insurance Society Limited.

This post is funded by RLAM